Free Capital

10 Lessons from 12 Private Investors

I’ll often wait for a book to get recommend multiple times before I become interested in reading it. Free Capital is such a book.

A friend had recommended it, I heard others speak of it, and in the process of completing my deep-dive on Ian Cassel, finding out he had written the foreword is what got me to purchase it.

I enjoyed reading the book very much. It’s short enough that I got through it in 1 week.

The book profiles 12 private investors based in the UK who decided to leave their careers to become full time private investors. Nearly all had a penchant for small caps, which added value to the relevance of their strategies for me.

Each investor had accumulated £1m or more from stock market investment. Given nearly all achieved this in their ISAs (the UK’s tax free investment vehicle) the yearly contribution maximums (capped at £20,000 per year) mean reaching £1m or more is arithmetically impossible without exceptional investment returns (average returns need to be 25%+ per annum).

Rather than provide a detailed summary of the book, I thought I would share the things that resonated with me most. I summarised this into 10 lessons.

I’m not giving out too much of the book in these lessons, hence, if you find this interesting, I suggest you pick up a copy. If you’re not much of a reader, you can get 75% of the value from the summaries at the end of each chapter, and the author’s final chapter.

#1 - Don’t take advice

Not a disclaimer, rather a standard commonality across investors in the book.

They don’t take advice from others, they make up their own mind.

Many highlight the weaknesses of wealth management companies, stockbrokers, tax advisors, and other professionals. Some are quite active on online forums, but mention they value discussions rather than opinions. Research from others may form the basis for a start towards further research of their own, but nothing more.

The best investors make decisions on their own. Warren Buffet commented on this early in his career when he observed:

I don’t seem to have very much influence on Walter. That’s one of his strengths: nobody seems to have much influence on him.

-Warren Buffet, referring to Walter Schloss (one of the investors of Graham-and-Doddsville)

#2 - It Should Be Fun

I resonated with all investors when they commented on this:

John: “I am never happier than when I am writing, thinking or talking about [investment].”

Or Peter: “I have never felt that investing is like working.”

Or Sushil: “To call it work is a travesty – I spend all day doing things I enjoy.”

The wider correlation point I took away is that with investing being so hard, success will come to you later than you imagined. Therefore, you have to love the journey. Only those that do love it, stick with it long enough to the see the benefits.

By the time they see those benefits, they realise the joy was in the journey. One of the investors concludes with a nice phrase (which David Gardner also likes to use):

At the age of 66, his aim is “to have an interesting life, rather than to make more money”.

#3 - Just the right level of research

“Time is a limited resource with strongly diminishing returns. The first hour you spend researching a company is much more important than the tenth hour.

-Vernon

A number of the investors in the book make a similar point, although articulated differently. The point being that there’s a cliff you’ll reach after a certain amount of research into a company. You want to find just the right balance, not too little, but not too much either.

Below is are two related takeaways from Bill:

Insights and Advice Wisdom as neglect

The art of being wise is knowing what to overlook. Selective attention Focus on the few most salient metrics and facts in any situation. Different metrics and facts are salient for different types of company and situation.

Substance over form

A focus on substance over form is probably more effective in investing than in most organisations or in public life.

#4 - Think

This is powerful one that I find particularly relevant in today’s context.

It’s easy to go through hours of research on a company and forming a thesis that’s nothing but a collection of other people’s work.

Spend time thinking. This will bring you to insights that are unique to you, those are rare and powerful.

“Most investors would have better performance if they thought more and did less. One of the great tricks in investment is learning to be happy doing nothing.”

#5 - Defensive optimism

Whilst I’m a true optimist at heart, and tend to dislike notions of pessimism in general (explaining why I’ve changed the name of this lesson), I resonated with the framing of one of the investors in the book, who explains defensive pessimism as such:

“It is always easy to think of reasons to buy a company. That is what most tipsters do.

To make good decisions, you need to look actively for reasons not to buy a company. And then invest only in those where you can live with those reasons.”

This is akin to Charlie Munger’s point:

“I never allow myself to hold an opinion on anything that I don't know the other side's argument better than they do”

― Charlie Munger

#6 - Go Long

This point is obvious, but this is where stories in the book shine, and are always so much more compelling than simple take-aways.

The book offers a lot of good accounts of some of the companies investors held positions in for years, and the benefits that came from those.

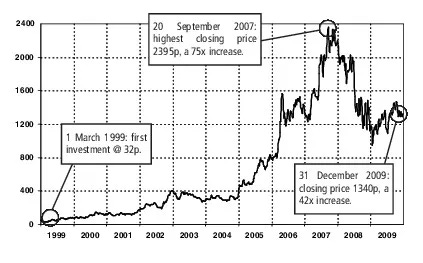

One of the investors, Luke, shares the thesis of his investment in Soco International. The media at the time was predicting the that long decline of the price of oil would continue. This got someone with a contrarian mindset, and a deep understanding of the industry (and cycles), to pay closer attention to what the general public may have been missing.

Here’s the visual story:

This is a 42 bagger that took 10 years in the making, and wasn’t timed perfectly. You increases your chances of success when you think long term.

The author shares this outstanding reality about another investor:

Very long holding periods in very successful companies have in a few cases led to him receiving an annual recurring dividend greater than the original total cost of the investment.

#7 - Hold cash

Nice an easy one. There’s always opportunities in the future, cash helps you seize them.

“It is a mistake to think of cash as burning a hole in your pocket.”

#8 - Don’t Diworsify Too Much

We hear this one from Buffet and Munger at every annual meeting.

It’s interesting to read from the book that some investors have portfolios of 40+ companies and consider themselves ‘concentrated’. Admittedly, that’s because the portfolio’s vast majority is weighted in the top 10 holdings. You likely know where the sweet spot is for you; the stories acted as good reminders.

When you find a good idea, buy enough to make a difference.

Diversifying away risk may also mean diversifying away profit.

#9 - Failure happens to the best of us

As with anything with a potential promise of great payoffs, investing is hard. In the final chapter, the author shares many lessons he’s picked up from the investors. This is one I observed throughout the book.

An unkind assessor might argue that several interviewees appear to have been career failures, albeit now financially successful failures.

No overnight success: Most interviewees went through a long initial period in which they were largely unsuccessful investors. They either broke even or regularly lost small amounts of money, but not enough to deter them from trying again.

#10 - Be a generalist

The book covers investors with vastly different styles, but I would say all are mostly generalists. They apply basic judgement and business principles to form their unique style. There’s nothing too crazy, and there’s no deep form of domain expertise at play.

Foxes, not hedgehogs

The philosopher Isaiah Berlin divided writers and thinkers into two categories, foxes and hedgehogs. These terms originate from a remark attributed to the Greek poet Archilochus: “the fox knows many things, but the hedgehog knows one big thing”.

Conclusion

Whilst I’m certainly not one to fly through one investment book after another, I do read a lot and picking up an investment book every quarter or so can be very valuable.

I will continue to share lessons from the next ones on the bookshelves. Feel free to share this with a mate who you think would enjoy it, and leave a comment with some of the books you value too.

Disclaimer

The content and data on this website is for information purposes only, and should not be read as investment advice, or advice on tax or legal matters. The companies and strategies discussed are on the site for entertainment only, we may or may not at any time be invested in the companies, and may be referencing companies simply as examples, ideas or for discussion.

By viewing the contents of this article, you agree:

(1) you have read and understood the warning and disclaimer above;

(2) not to make any decision based on the contents of the article;

(3) not to place any reliance on the contents of the article; and

(4) that the author is not responsible or liable, directly or indirectly, in any way for any loss or damage of any kind incurred as a result of, or in connection with, your use of, or reliance on, any of the contents of these articles.

Nice summary mate! I like ideas 3&4 in setting yourself a time to research but not too much time. Also thinking yourself and doing that research for yourself rather than borrowing ideas from others. Great to learn from the best, will add to the reading list!