Movers and Shakers in Q1🧂

My comments on 11 companies that moved this quarter

Well, we did it folks, the first quarter of the calendar year is behind us. Things were headed in the right direction in January, even the media was on our side.

“Since 1950, when the S&P 500 was positive in January, the rest of the year saw an average return of nearly 12%, with 86% of the returns positive” (ref here).

Afterwards is when the shit hit the fan.

The reporting season showed vulnerability that few were prepared to digest

SVB went down

Speculation about the direction of interest rates hikes continued

GPT-4 was officially launched

Elon pulled an Elon and changed the twitter logo to Dogecoin

Here we are today. Throughout all this, it feels like ages ago that the ASX said “see you layter” to Laybuy, but yeah, it happened.

Some companies did very well in Q1, others suffered. Let’s discuss some of these.

Winners 📈

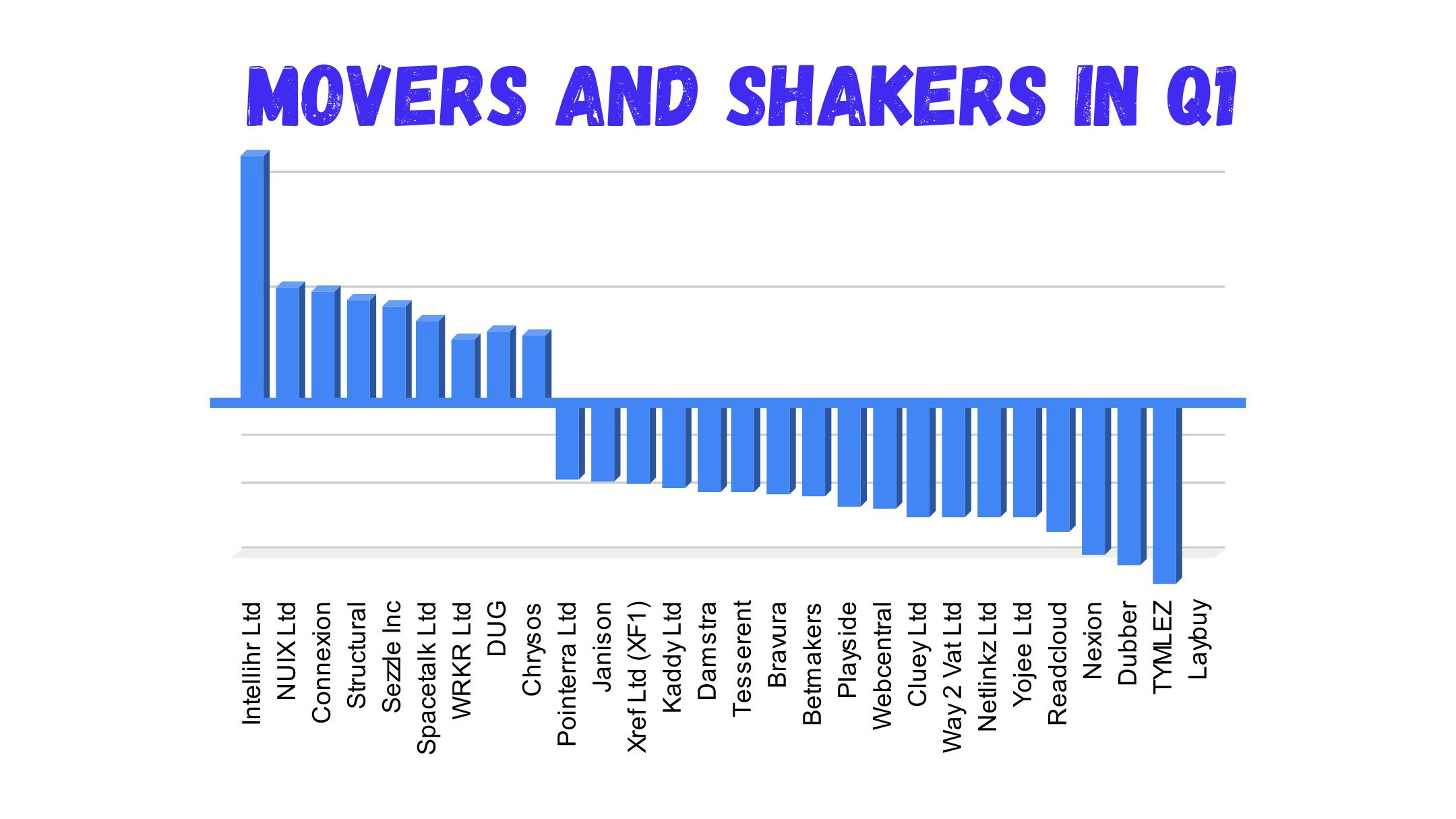

I’ve looked at companies that I follow from either close or afar who’s stock moved 50% or upwards. Here are 9 such companies:

1. Intellihr Ltd (IHR.ASX) +360%

What a story. The clear standout winner of Q1 in my book was IntelliHR. The fun continued long after I posted my opinion on what the beginning of the bidding war may have meant for valuations in this environment.

If you’re keen to learn more about the story, see my original post here.

I selfishly wish Intellihr had remained listed. Its growth had been phenomenal and the potential in the future seemed very large. Seeing it continue to expand, and benefit from the journey would have been nice. Oh well. Well done to leadership and the board.

2. NUIX Ltd (NXL.ASX) +104%

The data analytics and intelligence software provider had a rough ride since it’s listing; going from listing at $7.50, peaking at $11, and falling down to $0.60. Investors didn’t like the valuation to begin with and a downgraded guidance got them in the doghouse fairly quickly.

With the court case won and those dramas now behind them (link here), investors would have been happy with a small profit rather than a loss at half-yearly results, and signs of a potential turnaround might show.

I remain skeptical, but will keep tabs on these guys.

3. Connexion Telematics Ltd (CXZ.ASX) +100%

Little had happened in the last 4 years with the telematics software provider Connexion. A lot happened in one day when they announced that GM had agreed to extend the supply of their platform to all its courtesy transportation program. They mentioned this was forecasted to add Monthly Recurring Revenue of US$250k, which is fairly significant considering the size of the company.

It’s always been difficult with them to envision where future growth may come from given how mature and competitive this market is. I have seen the CEO, Aaryn Nania, present recently, and he seems to be the right calm and focused leader the company needs, so I will remain interested to see what they achieve in the near future.

4. Structural Monitoring Systems Plc (SMN.ASX) +91%

Sensor producer Structural Monitoring allows early identification of cracks in metal structures for airplanes. The chairman announcement at the beginning of the quarter that the first payment was received from Delta Airlines, and that they were now going to be in a position to apply to the FAA for formal certification. This would be a big turning point for the company.

The half-year results were strong with 51% revenue growth, and nearly flat on the bottom line. They are still burning cash, and start to appear low of it, so I wonder what will happen in the next few quarters. Let’s see how they go.

5. Sezzle Inc (SZL.ASX) +82%

BNPL player Sezzle provided a pleasing update in January, announcing that, for the second month in a row, Sezzle achieved profitability in net Income and Adjusted EBTDA.

For 4Q22, net income was US$0.5M compared to a net loss of US$25.9M in 4Q21. The company had said it would save US$70M, but the market had remained a little skeptical, now it seems we have evidence of execution.

The CEO Commented:

“Our team worked tirelessly towards implementing over US$70.0 million (annualized) in revenue and cost initiatives in 2022, resulting in profitability in 4Q22. We are also excited to announce that we have identified additional initiatives that we believe will drive another US$10.0 million in revenue and cost benefits to Sezzle.”

It will be interesting to see how this plays out in the next reporting season once the numbers show on the cash flow statement. As a result of these initiatives, active customers also went down 10%, which is likely a good thing (removing not so good customers), so let’s see if this can go back in the other direction in the future.

Losers 📉

Here’s the flipside of the coin:

1. Pointerra Ltd (3DP.ASX) -36%

After I posted my initial thoughts on why Pointerra was in the dog house (here), Bevan Slattery (under his Capital B Asset Management Trust) sold enough shares to exit the substantial shareholders list.

He did the same with IntelliHR, so perhaps it may have been nothing more than a move towards more liquidity, and an omen of good luck to come?

Pointerra should report its 4C and offer the much anticipated ACV update at the end of the month, until then, we remain in suspense. Can they me the comeback kid? We’ll see.

2. Janison Education Group Ltd (JAN.ASX) -37%

The digital assessment provider for the education sector went a little backwards in Q1. They updated the market with some good growth and EBITDA, but downwards movement with a bigger loss on the bottom line.

Cash in the bank seems a little thin for the current operating rate, so some investors might be worried about a potential raise being unavoidable.

With the business trading close to 5 year lows, and having grown relatively steadily over time, some are seeing this time as an opportunity. We saw the chairman buying shares, as well as Microequities Asset Management Group Ltd (ASX:MAM) becoming a substantial shareholder.

They will be a fun one to watch.

3. Betmakers Technology Group Ltd (BET.ASX) -42%

The wagering technology platform provider Betmakers saw its slide downwards continue in Q1.

Only a little bit of growth (7.5%), combined with a continued big loss (~$20M) may have been expected, but not welcomed.

The company announced a board and management restructure, by appointing Matt Davey as group president and executive chairman. Davey was a former member of the BetMakers board. He sold out of Betr to assume the leadership role. Former BetMakers CEO, Todd Buckingham, will now take the post of chief growth officer.

It was good to see Matt purchase shares on market, and the future will be interesting to watch to see if they can deliver on the profitability and sustainability they promise.

4. Netlinkz Ltd (NET.ASX) -50%

Cloud network provider Netlinkz went down in Q1.

Steady growth continued in their half-yearly (18% top line). Other wins were announced too, namely a reseller agreement with SpaceX. But the theme remains the same; VSN starlink will take capital to create and the market is worried about the little cash that remains in the bank for them.

Looks like Regal Funds Management may have exited the boat as well. Keen to see what the next few quarters hold for them.

5. Cluey Ltd (CLU.ASX) -60%

When the online tutoring and education provider released its December results, the steady growth continued, but cash burn was definitely worrying. They estimated 3 quarters left in the bank. Not wanting to chance it, they announced a $10M, raise which unsurprisingly sent the share price downwards.

The ex-CEO, now deputy chairman had been buying on market steadily in 2022 at much higher prices. With this latest raise, Thorney technologies have a substantial share of the business.

The question is: are they now good to go until cash flow profitability? It’s possible. I’ll be watching closely.

6. Dubber Corporation Ltd (DUB.ASX) -62%

Crazy to think Dubber peaked at a market cap north of $1B in September 2021.

Dubber have a good mission, what appears to be a valuable product (reviews here), but it’s hard to focus on much else when a company reports higher product manufacturing and operating costs than actual cash receipts from customers (saying nothing of staff and R&D expense).

A business restructure and review was announced on the day the half-yearly came out. They expect to be able to deliver $5M in savings per quarter. Very quick math would indicate this won’t be enough at the current pace.

I’m skeptical about the future, and would love to be surprised.

Conclusion

In the companies I follow, there was more movement to the downside than the upside in Q1.

With upcoming quarterly cashflow reports from many of these in 1 month, we’ll get a good sense of the business landscape in 2023. I remain hopeful that the later end of this calendar year could be positive, but a lot of uncertainty remains. Let’s wait patiently.

As always, feel free to challenge my opinion on these companies, share something I’ve missed, spotlight another big mover, and share the newsletter with a community; it’s free to sign-up.

Have a great Easter folks, see you on the flip side.

Disclaimer

The content and data on this website is for information purposes only, and should not be read as investment advice, or advice on tax or legal matters. The companies and strategies discussed are on the site for entertainment only, we may or may not at any time be invested in the companies, and may be referencing companies simply as examples, ideas or for discussion.

By viewing the contents of this article, you agree:

(1) you have read and understood the warning and disclaimer above;

(2) not to make any decision based on the contents of the article;

(3) not to place any reliance on the contents of the article; and

(4) that the author is not responsible or liable, directly or indirectly, in any way for any loss or damage of any kind incurred as a result of, or in connection with, your use of, or reliance on, any of the contents of these articles.