Volpara (VHT.ASX) : Deep Dive

We’re not going to replace the radiologist with AI, but we will replace the radiologist that doesn’t use AI

I thought it might be fun to be able to start this deep dive with nearly the same first sentence as the previous one (that’s how I make important decisions in life).

Born out of Wellington, New Zealand and now operating mainly from the USA, Volpara makes an AI-powered image analysis software that enables radiologists to quantify breast tissue and help produce better quality mammograms. This helps better understand cancer risk earlier, and plays an important part in guiding future recommendations and interventions.

I first read about them in the AFR 4 years ago, and must admit the founding story moved me.

What didn’t move me at the time was the price investors had to pay for the company.

Since then, the market’s re-rated cash-burning tech companies, and Volpara has delivered some quality growth.

Hence, I thought now would be a good time to get into the company and put some thoughts down on what to watch for in the future.

🖐 4 bullet Summary

The bull view: Volpara’s nascent strategy of targeting elephants helps them continue to win large US contracts. They leverage their new products to expand contract size, and continue growing in the 20-30% range for years to come.

What the market is missing:

True market penetration in the US is lower than perceived (estimated at 10%)

The potential upside from new, complimentary products.

Key risks: Well established competitive landscape. Democratisation of AI tools can lead to expansion of new entrants in the market. Cash burn continues. They have history of raising for acquisitions which could dilute shareholder returns.

The bear case: Failure to continue fast innovation leads to growth slowing down. With the company still “priced for growth”, they get downgraded.

History

The AFR article I mentioned above tells the ‘aha moment’ when the idea came about well:

When Ralph Highnam, the CEO of breast cancer specialist Volpara Health Technologies, was pursuing his PhD in artificial intelligence at Oxford University, he wanted to help people rather than improve factory robotics.

A late breast-cancer diagnosis for the mother-in-law of this Oxford professor – and fellow Volpara director – Mike Brady, propelled Mr Highnam to get his doctorate in engineering science, specifically in breast imaging.

"Mike said [breast] screens save lives, but it could be improved," Dr Highnam told The Australian Financial Review.

“I thought, wow ... This is an area where I can really help people.

"Breast cancer is not about an individual person, it really is about the family. I’m personally very tired of seeing younger women with kids being diagnosed with cancer. The fact is, if you can detect cancer early there is an exceptionally higher survival rate over five years."

It wasn’t a straight line to success from there though.

They tried to commercialise the technology after having worked on it, but found that clinical providers were years away from thinking about this.

So instead, Ralph pivoted to brain imaging which was more ready for AI. Mirada Solutions did very well, and after less than 3 short years, was acquired by CTI and then Siemens.

After a consulting stint, Ralph met with his professor Mike Brady once again in 2009. The decision was made that there was no time like the present, and Volpara was born.

This professor has done very well out of sharing one good idea, he remains on the cap table with a 2.63% stake in the business.

When Volpara listed in 2016, it reported $2.5M in revenue. Now 6 years later, their year end report is weeks away, and they appear to be on track to generate more than $30M in revenue.

🥊 What problem do they solve?

Stick with me for a short masterclass on breast health.

Breast cancer is the most common cancer in women. In Australia, one in eight women will develop breast cancer in their lifetime.

The traditional way to prevent this is screening with a mammogram every two years from the age of 50 (or earlier if your GP advises it). A mammogram is a lowdose x-ray of the breast tissue. It can show changes that can’t be felt during a physical examination.

The problem is that mammograms often can’t show you what you need to examine. Why? Because about half of the women that have mammograms have dense breast tissue, which makes it incredibly hard to visualise if there is cancer there.

Density is the #1 risk of developing breast cancer: the more density you have, the more place there is for cancer to develop. Also if cancer develops, it’s much harder to see. Hence, density both hides cancer, but is also a risk factor in and of itself.

This is the problem Volpara solves; their software improves the quality of the imagining, and uses AI to help radiologists understand risks better.

Products

Building on what I explained above, here’s a little more on how the product actually works.

Volpara now has 6 main products. I’ll explain the 3 most popular here.

Volpara scorecard

This is their first, cornerstone product. The technology works as an add-on to a mammogram:

A woman has an x-ray

the X-Ray machine sends her scan to Volpara's server

Volpara generates a breast density scorecard

This information is sent to the screening radiologists and to the cloud.

The service costs the imaging operator from $US2 to $US6 per woman.

The radiologists is now better informed to decide what’s the next best action; are we all good, or should an MRI be done?

Volpara Analytics

This is where they apply the power of a computer and AI to analyze the quality of a mammogram:

They analyse areas of the breast contrasted to a perfect image to be able to tell the quality of the image.

This contrast allows the operator to receive feedback.

This is important because instances where a woman gets a call saying her image isn’t viable creates stress (OMG, do I have cancer!?), and is costly for the clinical center.

Volpara Risk Pathways

This is a newer product to the company which came onboard via the acquisition of CRA Health.

This product allows the ability to either gather information from a patient portal, or gather their personal health record through epic.

They then run this through a proprietary algorithm, and calculate cancer risk. Variables taking into consideration are things like:

Family history of Cancer

BMI

The goal here is to give people a personalised plan to prevent them from cancer.

Moat

One of the many interesting things about Volpara is that unlike the majority of Saas companies I follow and understand, Volpara has trademarks, patents and regulatory approvals to protect its science.

I read 9 of them (here). With technology, there are ways around patents, but this will undoubtedly make it harder for competitors to move in their direction.

Having a scan on Google Scholar, research papers are plenty related to Volpara. This would help support buying decisions of their prospects, and elevate their authority in the market.

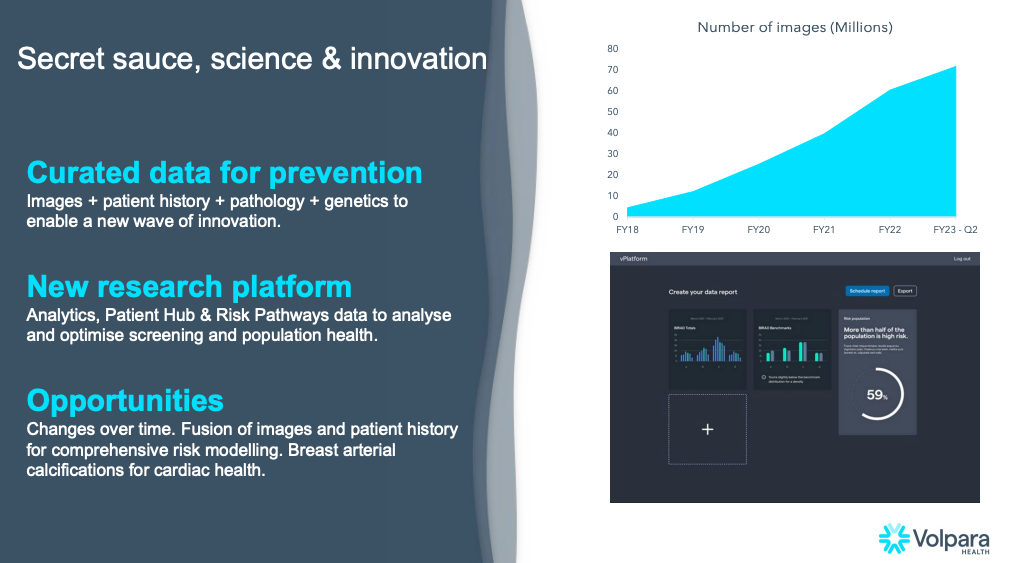

Secret Sauce

When they’re asked about their defensibility, Volpara often refers to the fact that they are the only ones (as far as they know), to do volumetric measurements. This means they use 3D images rather than 2D. This adds a lot of useful data to the capture, rendering the results more accurate.

This data helps radiologists, given studies show that radiologists they only tend to agree with their own analysis 75% of the time (source here).

Combined with this is the quantity of images they have in their database. More images means more data, more data means better model training, which means more accuracy. Some of their competitors may have thousands of images, whereas Volpara in 2022 claimed they had more than 65M images.

Tailwinds: Regulation

For years, Volpara had been commenting on increasing regulations in the US requiring mammography facilities to inform patients whether their breasts are composed of dense tissue.

States were slowly piling up and adding regulations individually. A big win for them came on the 10th of March 2023, when this regulation was finalised at the Federal level (announcement here).

This new ruling should be of significant benefit to Volpara, given nearly 40 million mammograms are performed each year in the US, and they estimate their software is used to assess the breast density of around 6 million annually.

Culture ⛷️

Volpara states in nearly every one of their presentations that they are a mission-driven organisation. On Glassdoor, they’re overall EPS score, at 3.7, is a little higher than IkeGPS, but not much more.

As I often mention when reviewing these, we have to be mindful of people’s emotional states when they fill these forms, but also be receptive to the feedback.

Comments are made about:

A commission structure that could be more favourable

The challenges of working across NZ to US timezones

“Focus and strategy continuously change”

It’s certainly not all doom and gloom. On the positive sides, notes around:

“I like the innovation here.”

"Work with highly talented and passionate people"

"Wonderful Coworkers Team atmosphere Benefits Good"

And indeed, a lot of positive comments made about the mission and vision

My outsider opinion is that they build on their mission nicely with relevant initiatives. I recently saw them announce on LinkedIn that they would donate 5% of the profits from all sales of its Volpara Scorecard™ breast density assessment software to DBI for the next twelve months (here).

Employees

Volpara stated it would reduce headcount in its effort to cut costs and reach break even faster. LinkedIn shows evidence of this:

A few quick notes:

The median tenure of 3.1 years is higher than I tend to see in tech, that’s a good sign.

New CEO mentioned they want to support their customers more (this will also allow upsells more easily), we can see evidence of this in the recent hiring:

Growth 📈

Evaluating Volpara’s growth is not necessarily a straightforward exercise, because they have acquired a number of businesses over the years to expand their platform.

Here’s what it looks like at a high level, using simply their appendix 4Es.

We can see rather explosive growth in the early days as they came off a small base, and now growth becomes more steady in the 30% range.

Future Growth

The interesting question is always what we can expect in future years.

To that end, here are some of the primary future growth levers:

Gaining more market share in the US: Whilst they often showcase in their marketing collateral a figure of 1/3 of US providers using Volpara, The CEO comments that few of their clients use more than 1 product. This leads them to estimate their ‘true’ market penetration at 10%. There’s room for growth here.

New products, primarily risk pathways: Risk pathways seems to be what they often lead with when they present. This new and unique product had a lot of potential, and can be upsold to clients using only Scorecard, or Scorecard and Analytics.

Products in development: They have announced about 1 year ago that they partnered with Microsoft to work on a better way to identify breast arterial calcification. This has a lot of potential upside, because women don’t tend to show the same signs as men prior to heart attacks, meaning the value of this would be impactful. This is still in development of course, so no guarantees a product comes out of it, but if it does, this could be a strong growth lever.

Additionally, leadership also talks about other cancers; pancreatic, colorectal. They might be well positioned to grow into those areas.

New markets: Volpara generates a portion of its revenue outside of the US, and they’ve mentioned that they expect other countries to slowly adopt more AI practices as well overtime.

They do not have a presence outside of APAC and the US, but through partners, growth could come from other regions.

Leadership 👩🏻💼

In April 2022, Volpara announced that Teri Thomas, a highly experienced healthcare industry executive, had been named the new group CEO.

The best part of this is that the founder, Ralph Highnam, would stay on as the Chief Science & Innovation Officer. He had enough with the bureaucracy, and wanted to focus on the parts that light up his fire; innovation (just my guess really).

Teri’s leadership style stands in stark contrast to Ralph. American, rather than English like Ralph, she’s quirky, direct, and seems to be winning the hearts of stakeholders with her strategy to target large accounts and focus on customer success. She’s a veteran in the healthcare IT industry, having spent 20-years at Epic, a global healthcare systems provider.

The numbers guru is CFO Craig Hadfield, who does a good job at answering questions on announcement calls.

Competitors 🤼

The span and depth of the platform has increased a lot over the years, meaning their competitive landscape is now more vast and fragmented.

Here are a few of their competitors I’ve either heard them mention, or found through my research.

Change Healthcare. They have a competitive product called Change Healthcare Mammography Plus™. Change is an American organisation with a very wide breath of solutions. It’s therefore hard to know how much of a focus promoting this product is for them.

Pro Medicus. 2 years ago, Pro Medicus announced that it had received FDA clearance for their Breast Density Algorithm. Whilst Pro Medicus’ track record of execution is nearly unmatched, the fact that their core business continues to grow strongly and bring in very large contract may mean the focus stays there. Only time will tell.

Hologic. They have a Breast Image Analytics, and are a mature and well established organisation. My quick spike on them seem to indicate that they are limited to 2D images, which would speak to Volpara’s edge over them. Note I could be wrong here.

Risks ⚠️

Like many other small cap tech stocks, two years ago, investors may have looked at Volpara thinking valuation alone was quite a large risk. In January 2020, Volpara traded at close to 30x sales.

Since then however, the revenue has grown, and the share price got re-rated, so this risk is now reduced, but of course, remains present.

The risks I see now are:

Priced for growth: building on the above, a casual observer could easily look at Volpara and deem it expensive. On the crude P/ARR ratio, they stand today at roughly 6x. (188M Market Cap, and $31M ARR (converted to AUD)).

This is by no means cheap in this current environment, and could be quickly halved, as we have seen happen to others, if growth gets obstructed in future years.

Cash Burn: Whilst it’s been great to see them deliver 2 consecutive quarters of positive cashflow, the CEO did mention not to expect this as the ongoing norm moving forward. They are enterprise sales led, do receipts will be lumpy, and I expect quarters of cash burn to continue to come up.

With ~$12M in cash remaining, I don’t see an immediate risk of needed to raise, but without certainty that FCF can be sustained, the risk here remains.

Competitive Landscape: I mentioned 3 of their larger competitors above, but with the more recent rise in AI tools available to all of us, I expect a potential of more entrants in the field in the next 5 years.

New entrants will have to work hard to chip at Volpara’s moat, but it’s not impossible that disruption happens and makes Volpara’s growth strategy harder to achieve.

Key leadership loss: For Volpara, given Terri remains relatively new, I would consider the loss of Ralph to be potentially more problematic.

Conclusion

My conclusion is that whilst Volpara is certainly not without risks, the upside for them is large if they can continue to execute.

I’ll remind you as always that this is article contains only my opinion, and nothing should ever be construed as financial advice.

For those of you interested to stay abreast of Volpara, given they operate on the NZ calendar, they typically release full year results at the end of May. Let’s see what they can achieve this year.

Thanks for reading all.

Feel free to leave a comment about things I missed, your contrarian opinion, or anything else relevant.

Other Deep Dives I wrote

Disclaimer

The content and data on this website is for information purposes only, and should not be read as investment advice, or advice on tax or legal matters. The companies and strategies discussed are on the site for entertainment only, we may or may not at any time be invested in the companies, and may be referencing companies simply as examples, ideas or for discussion.

By viewing the contents of this article, you agree:

(1) you have read and understood the warning and disclaimer above;

(2) not to make any decision based on the contents of the article;

(3) not to place any reliance on the contents of the article; and

(4) that the author is not responsible or liable, directly or indirectly, in any way for any loss or damage of any kind incurred as a result of, or in connection with, your use of, or reliance on, any of the contents of these articles.

Great read mate, well summarised and a company you can really get around and hope for its success.

Great summary. Nice work