10 Growers in FY23 - Part 2

[Part 2] 10 High-Growth Companies to Watch in the coming year

In last week's article, I looked into the financial performance of three companies. All of which scored above 50 on the Rule of 40. They were:

Camplify (ASX: CHL)

Vitura Health (ASX: VIT)

Vysarn (ASX: VYS)

Performance on the rule of 40 (using NPAT margins):

I examined the context behind their numbers and speculated on key factors to monitor in the coming year for these firms.

In this week's edition, we shift our focus to another set of companies that have exhibited robust growth in the current year.

#4 : Rectifier Technologies (ASX : RFT)

The company that makes reliable power supply solutions turned 30 years old in 2022.

It’s not the first time Rectifier shows up here. In March, I speculated that the market didn’t have confidence Rectifier would be able to continue delivering such strong growth. I suggested that explained why the share price didn't show significant movement.

Although the half-on-half growth was minimal, the company's ability to match the first-half results alone is impressive.

Reported figures:

The Opportunity

Large Contracts. As indicated in their final report, "the ASX announcement dated 16 November 2022, the Company has successfully secured purchase orders valued at USD 22 million from a critical customer." At that time, they stated, "The orders are expected to be fulfilled before the end of 2023 (calendar year)." However, management also hinted at experiencing manufacturing delays, leaving uncertainty regarding the extent of deliveries made thus far. Rectifier's ability to secure substantial contracts suggests the potential for significant future growth stemming from this agreement. More importantly to me however, it highlights their capability to secure and execute large-scale deals.

Valuation. As of today, with a Market Cap of $71.70 million and profits of $6.46 million, Rectifier's Price-to-Earnings (P/E) ratio stands at 11. This appears to undervalue a company that's demonstrating strong growth. The market is factoring in the uncertainty surrounding future growth prospects. If Rectifier continues its growth trajectory, there's a compelling opportunity for its valuation to move closer to a P/E ratio of 20. Such a valuation would be considered fair for a growing company with favourable industry tailwinds.

The anticipated expansion of EV charging stations is evident. Simply observing the increasing presence of EVs in our country over the past few years confirms this trend. Everywhere I look, I spot more Polestars, Teslas, and EV models from brands like Audi, Kia, BMW, and others. However, a significant challenge remains: the charging infrastructure lags behind this EV growth, (those living in apartment buildings without garages feel this pain sharply). This situation presents an opportunity for Rectifier, and if they execute their plans effectively, it could significantly benefit them.

Source: Statista Market Insights - Australia

The Challenges & What to look out for

Customer Concentration: By examining Rectifier's announcements, it's evident that they rely heavily on two major customers:

i-Charging (the USD $22M order mentioned earlier)

Tritium

While it's unclear what portion of this year's revenue these two customers contributed, it's undoubtedly a significant portion. This situation presents some risk. Additionally, the challenge lies in the depth of these relationships, as Rectifier hasn't provided an update on their partnership with Tritium in recent months. Drawing substantial conclusions from this is challenging, and we may need to await the Annual General Meeting (AGM) for further insights.

Inventories: Monitoring the growth in inventories can serve as an indicator of Rectifier's expectations regarding shipments to customers. This year, inventories increased from $5.8 million to $18.2 million. This growth surpasses the pace of their revenue growth, which could be viewed as a positive sign.

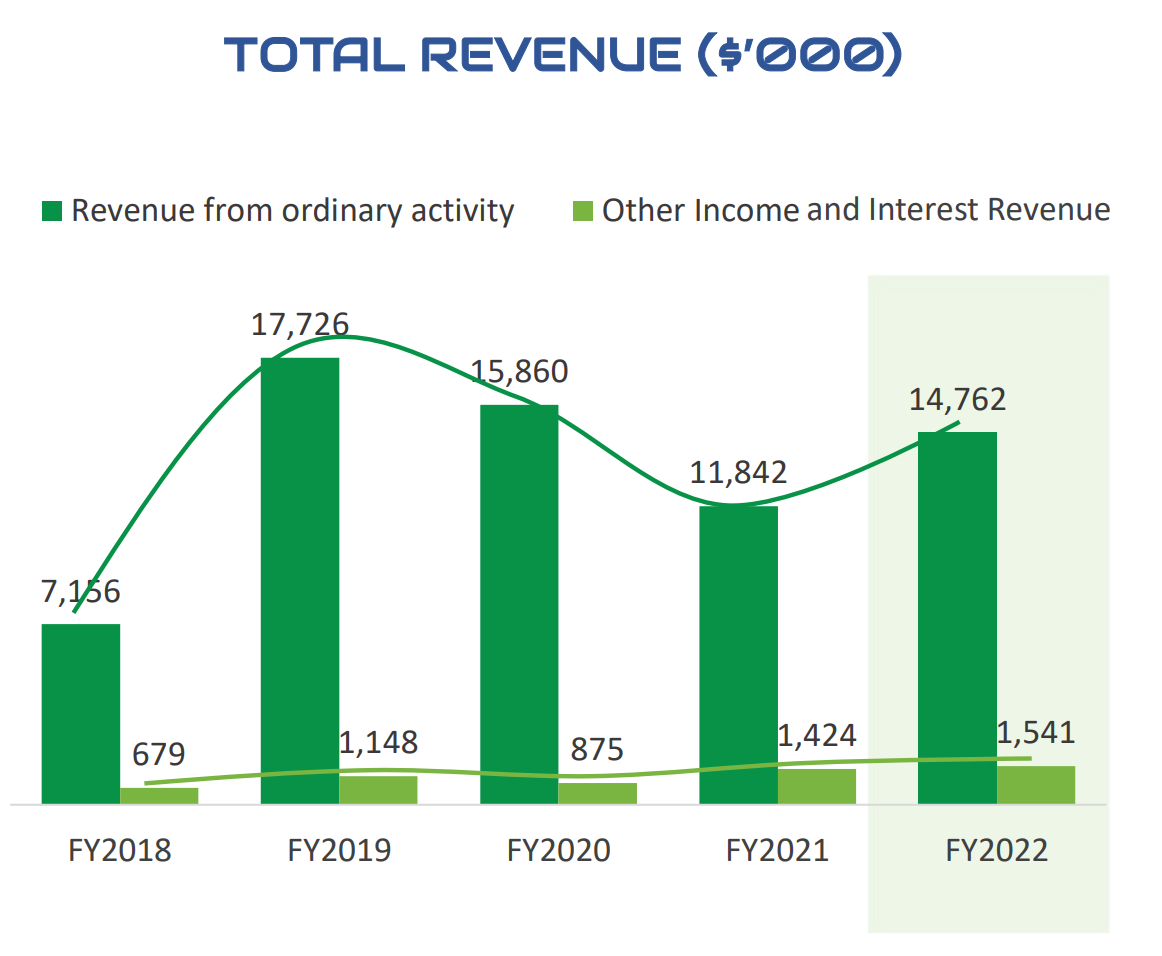

Future Growth: Building upon the points mentioned above, investors might be uncertain about Rectifier's potential for future growth. It's important to recognize that manufacturers typically don't experience linear growth like Software as a Service (SaaS) companies. Thus, brace for a potentially uneven journey, but also consider this year's strong performance as an indication that the company may be surmounting some of its recent challenges, as evidenced in the historical graph below.

Source: the company’s 2022 AGM presentation

#5 - Mad Paws (ASX: MPA)

I spotlighted Mad Paws in Business Models & Valuation, suggesting they were a good example of bolting on complimentary offerings, leveraging the power of the core marketplace. Whilst it’s still early days for them, this year’s strong results haven’t impacted the share price in the right direction.

What’s going on here? Let's look into it.

Reported figures:

This year’s 145% revenue growth was in part due to the Pet Chemist acquisition numbers. If we strip that out, we're left with a FY23 Pro forma revenue growth of +59%. This still represents robust growth, especially when considering the modest improvement in the bottom line. For me, the true gem in this business remains the marketplace, which I believe is the most compelling segment to watch.

The Opportunity

Scale: Mad Paws has attracted 46,000 new customers to its marketplace, marking a 30% growth this year. This highlights the inherent advantages of marketplaces—existing customers tend to return, and satisfied ones become brand advocates, reducing the need for extensive marketing expenses.

User Experience: While some negative reviews of Mad Paws exist online, the majority of users seem to adore the platform. Personal anecdotes and a solid average rating of 4.7 stars across 2,694 reviews on Product Review confirm this. Happy users are vital for their brand's growth.

The Challenges & What to look out for

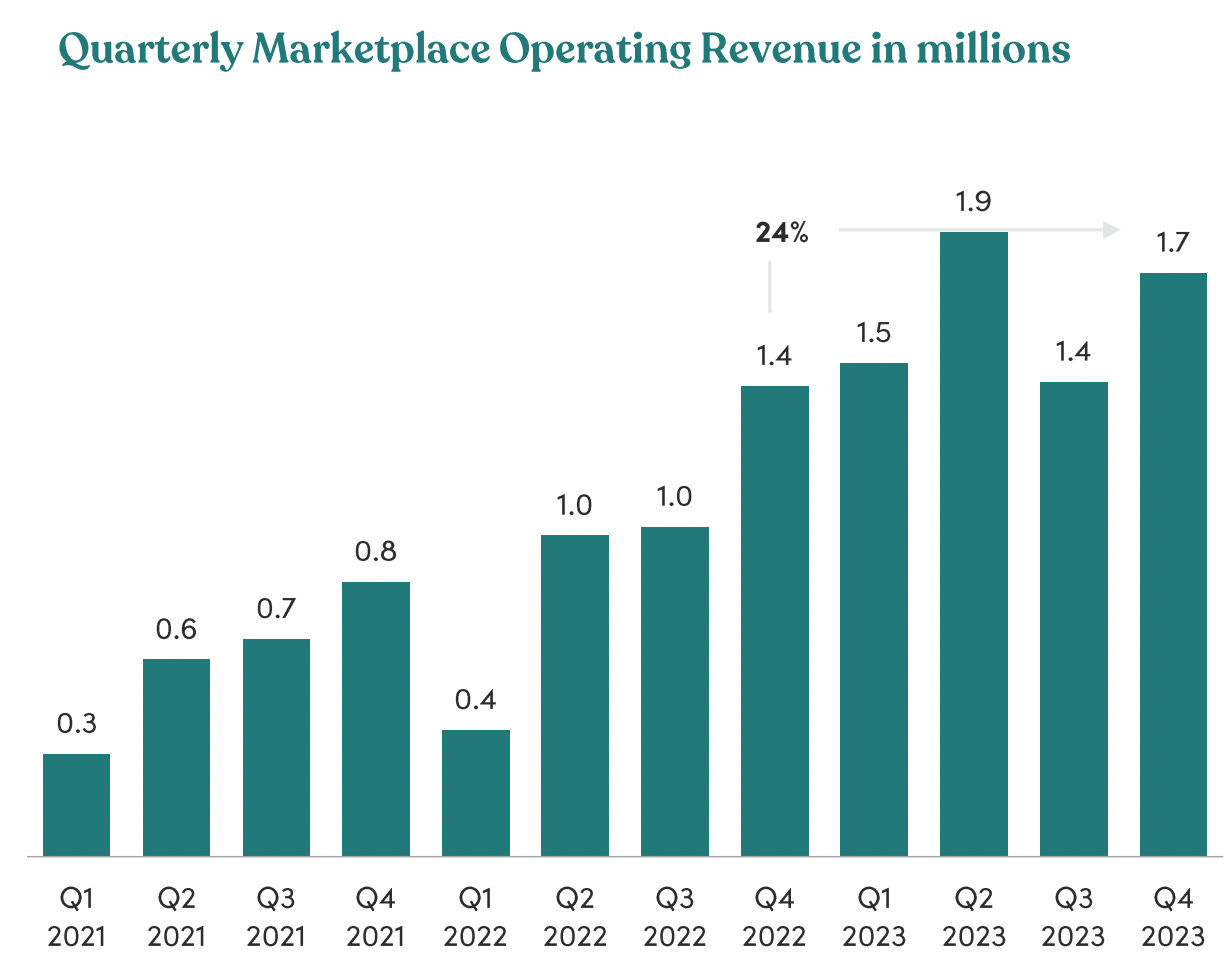

Growth plateau. While seasonal factors influence Mad Paws' performance, a quick look at their quarterly results suggests a potential growth plateau. Q4 performance remains 24% above the previous year's, but momentum appears to be tapering off. To their credit, the company has maintained marketing expenditure similar to the previous year, indicating that scale benefits are emerging. However, there's an argument for increased marketing spending to sustain growth.

Source: the company’s Q4 FY23 Update Presentation

Cap Raise. Although Mad Paws recently raised $4 million in February 2023, another capital raise seems inevitable. Examining last quarter's figures, the company operates with an approximate burn rate of $1.25 million per quarter (subject to seasonality). With only $3 million in current cash reserves, this covers just two quarters. As a CEO, ensuring sufficient cash is a job #1, and this impending capital raise may be exerting downward pressure on the share price. With $24 million in revenue and a market cap of $29 million, the company appears undervalued if it can avoid another raise, though that seems unlikely.

Growth unit economics change. As e-commerce outpaces the marketplace in terms of growth, the business's margin profile is changing. E-commerce typically doesn't achieve the high gross margins seen in marketplaces. This year, monitoring growth by segment will be essential to gauge the potential trajectory of each part of the business.

#6 - Acusensus Ltd (ASX: ACE)

Back in June of this year, Scott conducted an insightful deep dive into Acusensus. Max Wellth also wrote it up here.

While the company is gradually gaining the attention of investors, it remains in the early stages of discovery. Acusensus has had a standout year, surpassing its IPO prospectus projections and painting a positive outlook for the year ahead.

Reported figures:

The Opportunity

Large Contracts. Just before releasing its preliminary report, Acusensus announced the extension of its initial contract with Queensland. This expansion includes mobile phone and seatbelt monitoring (Heads Up). It's noteworthy that this extension added $10 million in contract value over five years, pushing the total contract value with Queensland to approximately $31 million. This suggests that similar contract extensions with other states are feasible. Below, we've included Scott's research findings from June for a deeper understanding:

US and UK largely untapped. Acusensus has been directing its efforts towards expanding in the U.S. and the U.K., where favorable market conditions appear to be aligning.

Regarding the U.S., they've noted that many states have submitted requests for Federal funding to access Acusensus' mobile phone and seatbelt enforcement services. Observing how this unfolds over the coming years will be intriguing.

In the U.K., they've done a good job at hiring Geoff Collins, a prominent local road safety leader. Their report indicates, "Further demand for Acusensus services in the UK is anticipated in FY24 and beyond," and "Acusensus anticipates the European tender will lead to other opportunities for mobile phone enforcement services in the region from FY25" (Source: Company’s Full Year Results Presentation).

The Challenges & What to look out for

AU market tapping out. At the risk of contradicting myself, I’m not certain how much growth the company can generate in the region. Perhaps my logic is too simplistic, but the states with the largest population (VIC,NSW,QLD), therefore largest traffic, would be the most likely to invest in this technology. These states may have made the larger part of their investment already. Hence supporting the need of international expansion. The counter to this is that these states may well decide to expand their use beyond the metro areas, and good growth may remain in them, but that seems less plausible to me.

New geographies may not be as easy. In a presentation hosted by NWR, the CEO discussed differences in the adoption of their technology between the U.S. and Australia. Although it's promising to see North Carolina as the first U.S. state to implement a mobile phone and seatbelt enforcement program for commercial vehicles, it suggests that the U.S. market may evolve more slowly. Convincing government agencies to adopt new technology can be a formidable task, even though Acusensus seems well-positioned for success. It might be a case of this endeavor taking longer than anticipated, as is often the case in enterprise sales.

Conclusion

There you have it—three strong contenders on our list of growth companies. Stay tuned for next week's edition where we'll dive into the final four impressive growers.

Your suggestions and insights are invaluable, so don't hesitate to share them in the comments. If you're tracking other promising small-cap growers that meet the Rule of 40, I encourage you to share your discoveries with our community.

I always appreciate your feedback, which helps me continue to deliver content that matters to you.

Disclaimer

The content and data on this website is for information purposes only, and should not be read as investment advice, or advice on tax or legal matters. The companies and strategies discussed are on the site for entertainment only, we may or may not at any time be invested in the companies, and may be referencing companies simply as examples, ideas or for discussion.

By viewing the contents of this article, you agree:

(1) you have read and understood the warning and disclaimer above;

(2) not to make any decision based on the contents of the article;

(3) not to place any reliance on the contents of the article; and

(4) that the author is not responsible or liable, directly or indirectly, in any way for any loss or damage of any kind incurred as a result of, or in connection with, your use of, or reliance on, any of the contents of these articles.